By this point in 2018, you should have heard of the term Blockchain. It’s been on the cover of magazines, nightly news, and has been discussed by high ups in both the private and public sectors looking to utilize this new tech. There is a big misunderstanding of what blockchain can and cannot do. As seen with cryptocurrency, you saw the abuse of the term of blockchain to solve all of life’s problems. Hundreds of Initial Coin Offerings’ (ICO) white papers explained how their use of blockchain will solve it all. That’s just not true.

In its simplest form, a blockchain is a set of distributed databases. They’ve actually already existed for a while; it’s just recently the term gathered all the hype around it with the rise of Bitcoin and other cryptocurrencies. So why is Blockchain high up on the hype cycle? Well after the 2014 crash of Bitcoin, smart money and players who weren’t already in the space started to see the value of Bitcoin’s blockchain, which is immutable, meaning it’s tamper proof. They saw this translating to a vast array of businesses whether it is logistics, insurance, titles, real estate, etc. The difference between Bitcoin’s blockchain (open, public chain), and a private (closed) blockchain like J.P. Morgan’s Quorum comes down to immutability. One is very hard to change, the other is easily changed with very little cost. The cost to change Bitcoin comes out to millions of dollars between electricity costs, hardware, and other associated costs to perform an attack on the network otherwise known as a 51% attack, as to gain control of consensus. Gaining control of consensus would allow one to double spend, reverse transactions, among other things. On a private blockchain, there are no costs associated, as there are no miners incentivized with keeping the network functioning. Thus the cost of changing something on Quorum is tiny compared to the cost of Bitcoin, so it comes down to who has access to the network and are they trusted with it. This is because Quorum like other private blockchains is tamper evident, meaning you will notice that someone changed an input, but you can’t prevent it as there is no consensus mechanism involved that makes it tough to attack.

“It’s important to remember that if there was no Bitcoin, there would be no blockchain.”

- CFTC Chairman J. Christopher Giancarlo

This was from his testimony on Capitol Hill which was held by the Senate Committee on Banking, Housing, and Urban Affairs back on February 6th. The statement itself couldn’t be any truer.

At a time where we see a divide between open and closed chains, I think we will head down the path of open chains down the line. Just look at the internet versus intranet. In the early 1990’s, many companies started to create their own intranets to communicate within the company. The internet was still a scary space to many then and a lot was still to be discovered. Intranets offered a lot of benefits including communication (allowing teams to communicate in real time across various sites and continents), workforce productivity (intranets help locate information and facilitate the flow of information much faster than previous technologies), and time (intranets allow users to access info on an as-needed basis.) So there are some upsides to having a closed network, but as we can see the term intranet is hardly used in comparison to the internet, which is constantly scaling as more users and data are thrown at it.

Every company now has a website, Twitter, Instagram, Facebook page, and more because it is so vital in today’s world. If your company isn’t on the internet and social media, it will fall behind as more and more user attention is shifting from the television to smartphone, tablet, and PC.

So in the not too distant future the same will be said for companies that operate on a public blockchain versus a private one that limits access to a few.

The biggest area that is looking to trim fat is going to be financial markets, where settlement currently is two days (regular way settlement), unless it is a cash settlement, which is the same day. It’s 2018, yet the majority of the financial world is still stuck in 1988. Bonds are still settled over the phone on paper. “Electronification” is changing markets across the globe and the major laggard has been fixed income markets (bonds.) This will allow for more automated trading (AT) and High Frequency Trading (HFT) strategies toward the fixed income market. These trading initiatives are looking to add liquidity to a market that is very illiquid to begin with, corporate bonds. Giving liquidity in the combination with tokenization will allow markets to be open 24/7 with minimal human interference. The advantage of the tokenization is clear, adding volume to the market and improving market quality – the ability to transact at prices that accurately represent the instrument being traded and being able to do so with immediacy. With increased liquidity, the hope is for ease of trade which would allow higher volumes to be traded with less effect on the price of the asset.

Simple things like settlement and tokenization of securities will vastly improve the securities market which is still slow and only open a limited amount of hours. Current U.S.-based exchanges like NASDAQ and NYSE are open 9:30 A.M. to 4 P.M. EST Monday through Friday, with some very limited after-market hours. ForEx and commodities markets are open 24/5 now, which is Sunday 5 P.M. EST through Friday 5 P.M. EST. For a U.S.-based stock owner, it is tough to trade after hours or over-the-counter (OTC) easily at the moment. But imagine a future where the shares of the company you own are tokenized. Now, you and your friend Bob could exchange shares of companies for cash, Bitcoin, or other shares if you wanted. Say your friend Bob owns ten shares of Apple. You ask to buy two of them off him for a grand total of $360. You give Bob the cash and he sends you two shares of Apple over a blockchain layer which settles the transaction. Now the ledger has Bob down for eight shares of Apple and two shares for yourself.

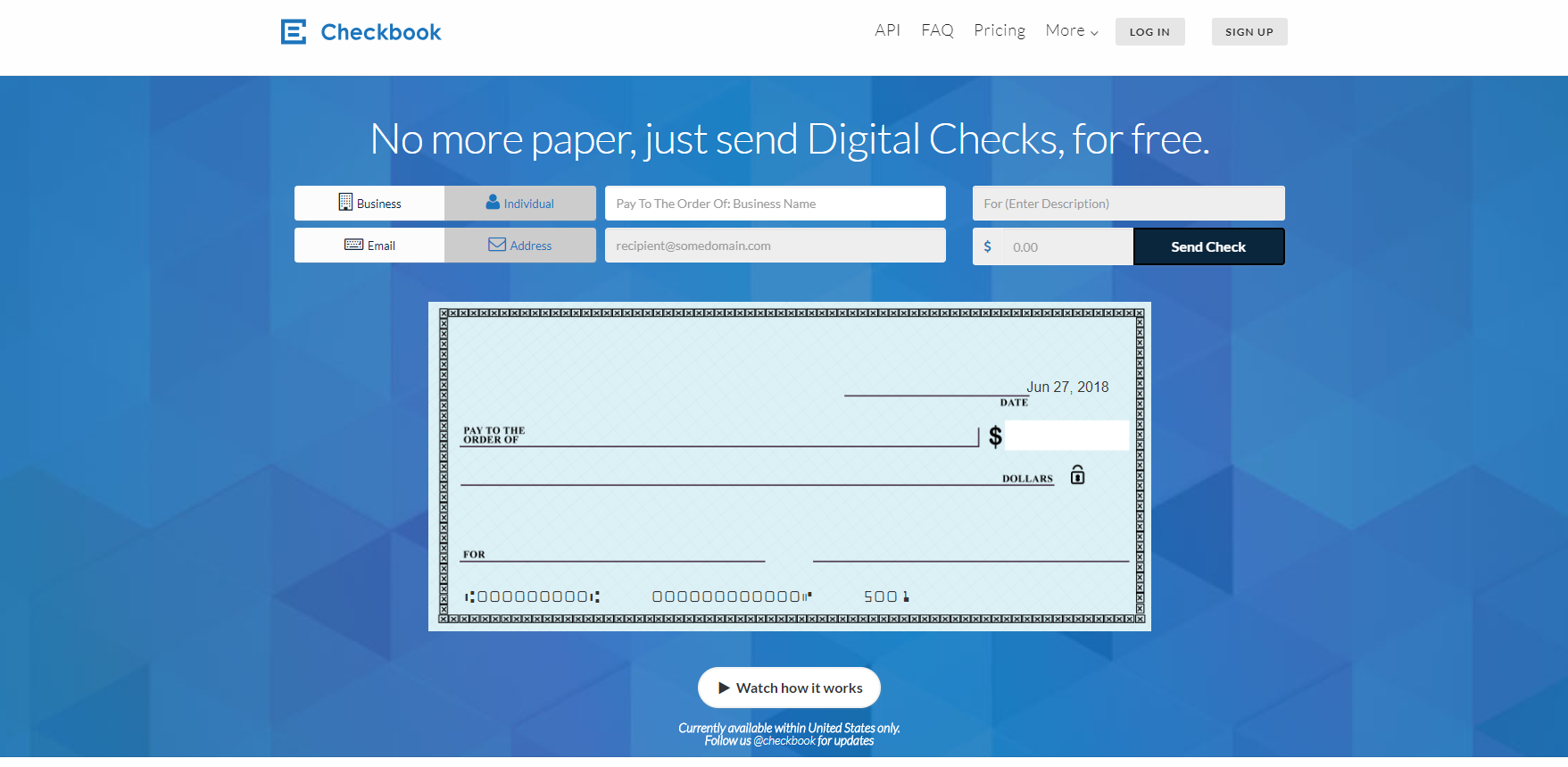

Checkbook – Implementing Blockchain for Instant Transactions

Recently I had the pleasure of speaking with both the founder, PJ Gupta, and director of marketing Jake Mastrandrea on this relatively new company (launched in early 2016). The company was founded on the idea of simplifying check deposits that are still slow, yet many people still use checks to this very day. In 2017 there were 17 billion paper check payments. The FED report from 2013 had paper check payments declining at nearly 2 billion each year for the ten-year period leading up until then. From 30 billion in 2003 to 19.7 billion in 2013. Data had shown by 2017 with the trend we had we would be in the neighborhood of around 12-13 billion checks annually. Turns out that checks are now disappearing 60% slower than they were before. This is where Checkbook found its niche.

The process to use Checkbook is simple: you go to their homepage, enter the check information into the very friendly User Interface (UI), and bam, you get an email asking you to confirm whether or not you wanted to deposit this check. Once your email is used once, future checks deposit automatically. Typically the check will deposit overnight or in two business days, versus ACH (Automatic Clearing House) which takes three days. Checkbook allows businesses to move away from paper to deliver checks right to a recipients email. In the modern financial landscape, fraud has become easier than ever. It seems every night the local news will run some story on a scam that some people are running on the internet because they are pulling payments. With Checkbook, payments are pushed, meaning that they do not credit accounts until the recipient confirms. Furthermore, the recipient doesn’t need to sign up to any service, download an app, or do anything; they simply just need to confirm the first email. Checkbook is not only solving the sender side, but also the recipient side of the payment problem. Digital checks can can be deposited and cashed online after instantly verifying your banking credentials with one of our partner banks. Checkbook is currently available in the United States.

Investors in Checkbook include Tim Draper, who is a legendary American venture capitalist, one of the first to big VCs to go head first into Bitcoin and other blockchain tech. With this kind of backing, you know Checkbook is up to something right.

There’s got to be a cost, right? Yes and no. For consumers, it is free. So if your mom gave you a check, it would cost her nothing to deposit it through the website. For businesses, it costs one dollar, no matter the check size. This is how Checkbook generates revenue via Business to Business (B2B) and via Business to Consumer (B2C). Checkbook allows businesses to simplify the process of sending checks or receiving payments. Think about how many times a company like AT&T or Verizon has to send refund checks out; now the process can run much smoother.

A person may ask what makes Checkbook any different than the numerous payment rails out there like Venmo or PayPal. Well for one, as mentioned earlier, it is a simple one-dollar fee per check for businesses versus PayPal where it is a percentage-based fees, so Checkbook is set to handle larger transaction sizes.

A fundamental difference between Checkbook.io and other payment systems e.g Paypal etc. is the recipient does not need to sign up or download yet another app i.e. no need to create another username/password.

Also, there are no on boarding fees or miscellaneous fees. Along with that Checkbook doesn’t hold users funds, like in PayPal how they have a wallet. This means the recipient gets their funds directly to their bank account.

During our talk, we discussed how Checkbook is implementing a closed blockchain of their own to go from an overnight settlement to instant settlement. The one problem (not even a problem, but more trying to improve their service) they are facing is getting a faster settlement and they couldn’t have found a better time to be in their shoes with the growth in blockchain awareness and development. Many companies are looking for ways to leverage the power of blockchain now that we’ve seen what it can do and time, money, and headaches it will save. It won’t be long before every electronic transaction is settled via blockchain whether closed or open chain.

The future of blockchain based settlement is looking bright to fuel all types of innovative companies like Checkbook.

Disclaimer: The views expressed in this article are solely the author or analysts and do not represent the opinions of the author, or Inflluencive, on whether to buy, sell or hold a particular cryptocurrency, cryptographic asset, stock, or any investment vehicle. Individuals should understand the risks of trading, investing, and consider consulting with a professional. Various factors can influence the opinion of the analyst as well as the cited material. Investors, traders, and others should conduct their own research independent of this article before purchasing any assets. Past performance is no guarantee of future price appreciation.

This is a Contributor Post. Opinions expressed here are opinions of the Contributor. Influencive does not endorse or review brands mentioned; does not and cannot investigate relationships with brands, products, and people mentioned and is up to the Contributor to disclose. Contributors, amongst other accounts and articles may be professional fee-based.